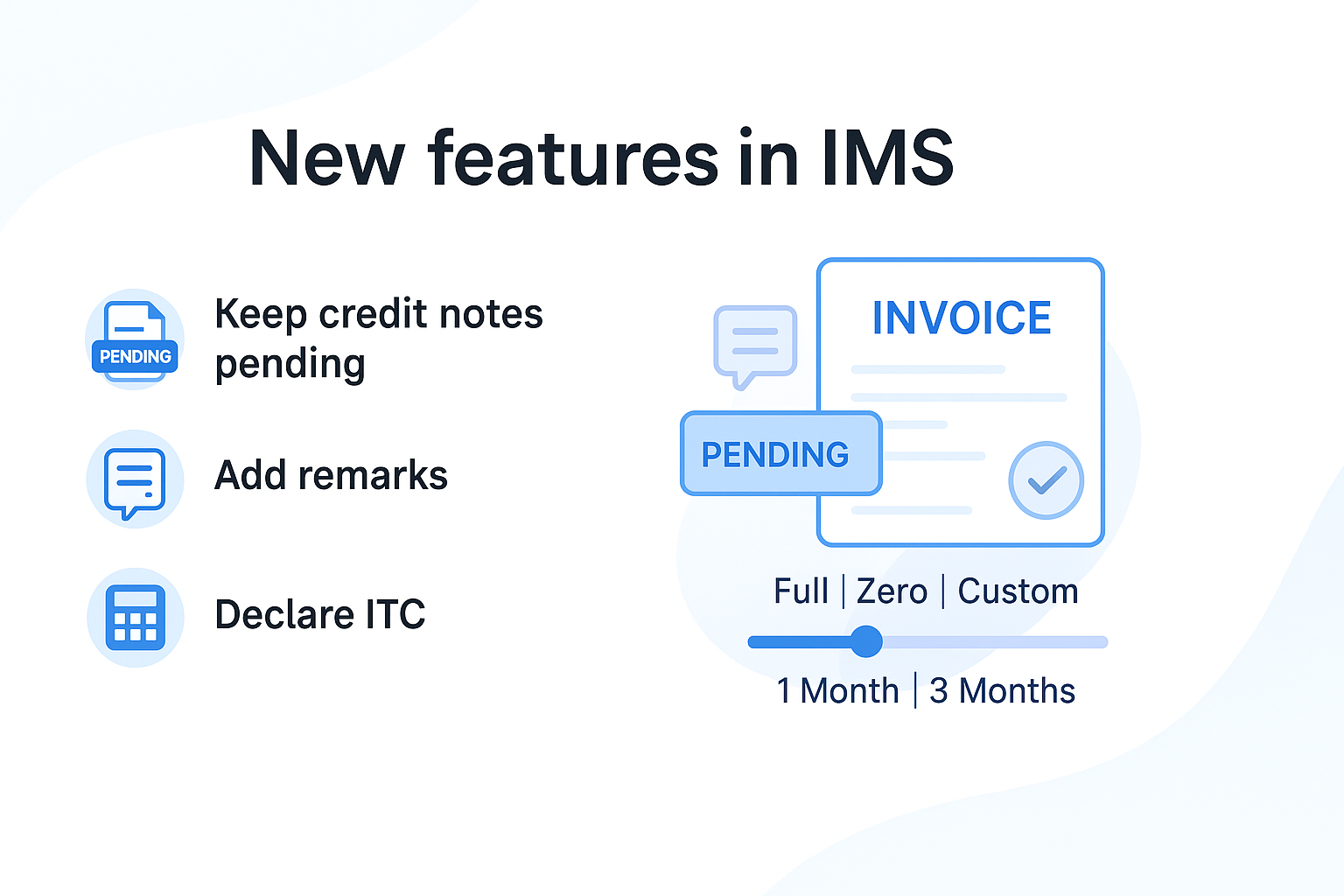

Recent changes in Govt Portal introduced the facility to keep credit notes pending in IMS for a limited period and ability to specify the amount of ITC reversal. To align Octa with these changes, Octa’s Inward IMS module has been updated for the following changes.

Keeping Credit Notes Pending

Imagine your supplier has issued a credit note that now appears in your IMS. However, you haven’t yet recorded (booked) this credit note in your books. When you run reconciliation, this credit note will be flagged as “Missing in Books”. In such a case, you have the following options:

- Reject: This will increase the supplier’s liability in GSTR-3B. However, this is incorrect because the supplier has rightly issued the credit note.

- Accept: This will reduce your ITC in the same month, even though the credit note hasn’t been booked in your records yet. This creates a mismatch during reconciliation.

Both these options are not ideal. To handle such cases correctly, the GST Portal now provides an option to keep the credit note pending for one tax period where tax period is defined as below.

| Filing Frequency | Tax Period |

|---|---|

| Monthly | 1 month |

| Quarterly | 3 months |

Credit notes can be kept pending for only one tax period. If no further action is taken, these credit notes will be automatically deemed accepted in the next tax period.

You can use the “Keep Pending” option for all cases where accepting a document would reduce ITC in GSTR-3B, such as:

- Credit notes

- Upward amendment of credit notes

- Download amendment of invoices

- Download amendment of debit notes

Adding Remarks

The IMS allows you to accept, reject, or keep a document pending. However, when you reject a document or keep it pending, the supplier may not understand the reason behind your action.

To improve clarity and communication, you can now add an optional remark while performing these actions. This remark will be recorded in IMS and made visible to your supplier in their outward IMS, ensuring transparent and efficient communication between both parties. In short, remarks help maintain a clear audit trail and foster better collaboration on document-related actions.

Declaration of ITC

In certain cases, the net ITC (Input Tax Credit) in GSTR-3B gets reduced. Some common examples include:

- Credit note

- Upward amendment of credit notes

- Downward amendment of invoices

- Downward amendment of debit notes

However, there are situations where a credit note is issued against an invoice on which you either:

- did not avail the ITC, or

- have already reversed the ITC.

In such cases, accepting the credit note will incorrectly reduce your ITC again in GSTR-3B. On the other hand, rejecting the credit note would increase the supplier’s liability — which is also not ideal.

To address this, you can now declare how much ITC should be reduced in GSTR-3B for such documents. Octa GST provides three options for ITC declaration:

- Full – Reduce full ITC amount (same as before)

- Zero – No ITC reduction

- Custom – Reduce ITC by a specific declared amount

Full

In this case, GSTR-3B will consider the entire ITC for reduction. That means the full amount will be subtracted from the net ITC of GSTR-3B.

Example:

| Document | Document No | Taxable Value | IGST | IMS Action | Declared ITC |

|---|---|---|---|---|---|

| Invoice | INV123 | 200 | 36 | Accepted | NA |

| Credit Note | CN451 | 100 | 18 | Accepted | Full |

Net ITC in GSTR-3B = 36 - 18 = ₹18

Zero

In this case, GSTR-3B will not consider any ITC reduction. This means net ITC of GSTR-3B will not be reduced for such documents.

Example:

| Document | Document No | Taxable Value | IGST | IMS Action | Declared ITC |

|---|---|---|---|---|---|

| Invoice | INV123 | 200 | 36 | Accepted | NA |

| Credit Note | CN451 | 100 | 18 | Accepted | ZERO |

Net ITC in GSTR-3B = 36 - 0 = ₹36

Custom

In this case, you can declare a specific ITC amount to be reduced. The reduction in GSTR-3B will be limited to the amount you specify. This is useful when you availed or reversed partial ITC against original invoice.

Example:

| Document | Document No | Taxable Value | IGST | IMS Action | Declared ITC |

|---|---|---|---|---|---|

| Invoice | INV123 | 200 | 36 | Accepted | NA |

| Credit Note | CN451 | 100 | 18 | Accepted | Custom: ₹12 |

Net ITC in GSTR-3B = 36 - 12 = ₹24

Please note that you can declare the ITC only if you accept the credit note.

Summary

The latest update to Octa GST’s Inward IMS module introduces key enhancements aligned with recent changes on the GST Portal. Users can now keep supplier credit notes pending for one tax period, preventing premature ITC reduction and improving reconciliation accuracy. A new remarks feature allows users to record reasons when rejecting or keeping documents pending, ensuring transparency for suppliers through outward IMS. Additionally, the new ITC declaration feature lets users control how much Input Tax Credit is reduced in GSTR-3B — with options to declare it as Full, Zero, or Custom — providing greater flexibility, accuracy, and compliance in GST reporting.